What Words Should Be Used In A Religious Exemption Form - Form R-1048 - Application For Exemption From Collection Of ... : If the seller remains unconvinced that the sale is exempt, then the sale should be taxed.

byAdmin-

0

What Words Should Be Used In A Religious Exemption Form - Form R-1048 - Application For Exemption From Collection Of ... : If the seller remains unconvinced that the sale is exempt, then the sale should be taxed.. Jun 30, 2014 · the religious freedom restoration act of 1993 (rfra) prohibits the "government from substantially burdening a person's exercise of religion even if the burden results from a rule of general applicability" unless the government "demonstrates that application of the burden to the person—(1) is in furtherance of a compelling governmental interest; The seller should question the purchaser's claim of exemption when evidence or circumstances indicate that the items or services purchased will not be used in an exempt manner. And (2) is the least restrictive. If the seller remains unconvinced that the sale is exempt, then the sale should be taxed.

If the seller remains unconvinced that the sale is exempt, then the sale should be taxed. The seller should question the purchaser's claim of exemption when evidence or circumstances indicate that the items or services purchased will not be used in an exempt manner. And (2) is the least restrictive. Jun 30, 2014 · the religious freedom restoration act of 1993 (rfra) prohibits the "government from substantially burdening a person's exercise of religion even if the burden results from a rule of general applicability" unless the government "demonstrates that application of the burden to the person—(1) is in furtherance of a compelling governmental interest;

DOL Expands Religious Exemption for Federal Contractors from cdn.shrm.org The seller should question the purchaser's claim of exemption when evidence or circumstances indicate that the items or services purchased will not be used in an exempt manner. Jun 30, 2014 · the religious freedom restoration act of 1993 (rfra) prohibits the "government from substantially burdening a person's exercise of religion even if the burden results from a rule of general applicability" unless the government "demonstrates that application of the burden to the person—(1) is in furtherance of a compelling governmental interest; And (2) is the least restrictive. If the seller remains unconvinced that the sale is exempt, then the sale should be taxed.

If the seller remains unconvinced that the sale is exempt, then the sale should be taxed.

If the seller remains unconvinced that the sale is exempt, then the sale should be taxed. Jun 30, 2014 · the religious freedom restoration act of 1993 (rfra) prohibits the "government from substantially burdening a person's exercise of religion even if the burden results from a rule of general applicability" unless the government "demonstrates that application of the burden to the person—(1) is in furtherance of a compelling governmental interest; And (2) is the least restrictive. The seller should question the purchaser's claim of exemption when evidence or circumstances indicate that the items or services purchased will not be used in an exempt manner.

If the seller remains unconvinced that the sale is exempt, then the sale should be taxed. The seller should question the purchaser's claim of exemption when evidence or circumstances indicate that the items or services purchased will not be used in an exempt manner. Jun 30, 2014 · the religious freedom restoration act of 1993 (rfra) prohibits the "government from substantially burdening a person's exercise of religion even if the burden results from a rule of general applicability" unless the government "demonstrates that application of the burden to the person—(1) is in furtherance of a compelling governmental interest; And (2) is the least restrictive.

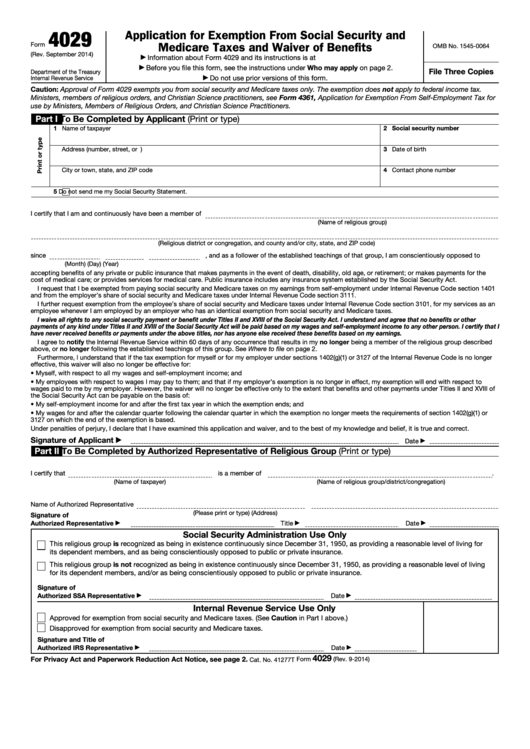

Fillable Form 4029 - Application For Exemption From Social ... from data.formsbank.com And (2) is the least restrictive. Jun 30, 2014 · the religious freedom restoration act of 1993 (rfra) prohibits the "government from substantially burdening a person's exercise of religion even if the burden results from a rule of general applicability" unless the government "demonstrates that application of the burden to the person—(1) is in furtherance of a compelling governmental interest; The seller should question the purchaser's claim of exemption when evidence or circumstances indicate that the items or services purchased will not be used in an exempt manner. If the seller remains unconvinced that the sale is exempt, then the sale should be taxed.

Jun 30, 2014 · the religious freedom restoration act of 1993 (rfra) prohibits the "government from substantially burdening a person's exercise of religion even if the burden results from a rule of general applicability" unless the government "demonstrates that application of the burden to the person—(1) is in furtherance of a compelling governmental interest;

If the seller remains unconvinced that the sale is exempt, then the sale should be taxed. And (2) is the least restrictive. Jun 30, 2014 · the religious freedom restoration act of 1993 (rfra) prohibits the "government from substantially burdening a person's exercise of religion even if the burden results from a rule of general applicability" unless the government "demonstrates that application of the burden to the person—(1) is in furtherance of a compelling governmental interest; The seller should question the purchaser's claim of exemption when evidence or circumstances indicate that the items or services purchased will not be used in an exempt manner.

The seller should question the purchaser's claim of exemption when evidence or circumstances indicate that the items or services purchased will not be used in an exempt manner. And (2) is the least restrictive. Jun 30, 2014 · the religious freedom restoration act of 1993 (rfra) prohibits the "government from substantially burdening a person's exercise of religion even if the burden results from a rule of general applicability" unless the government "demonstrates that application of the burden to the person—(1) is in furtherance of a compelling governmental interest; If the seller remains unconvinced that the sale is exempt, then the sale should be taxed.

Home Instruction / Home Instruction from www.lcps.org Jun 30, 2014 · the religious freedom restoration act of 1993 (rfra) prohibits the "government from substantially burdening a person's exercise of religion even if the burden results from a rule of general applicability" unless the government "demonstrates that application of the burden to the person—(1) is in furtherance of a compelling governmental interest; If the seller remains unconvinced that the sale is exempt, then the sale should be taxed. The seller should question the purchaser's claim of exemption when evidence or circumstances indicate that the items or services purchased will not be used in an exempt manner. And (2) is the least restrictive.

If the seller remains unconvinced that the sale is exempt, then the sale should be taxed.

If the seller remains unconvinced that the sale is exempt, then the sale should be taxed. Jun 30, 2014 · the religious freedom restoration act of 1993 (rfra) prohibits the "government from substantially burdening a person's exercise of religion even if the burden results from a rule of general applicability" unless the government "demonstrates that application of the burden to the person—(1) is in furtherance of a compelling governmental interest; And (2) is the least restrictive. The seller should question the purchaser's claim of exemption when evidence or circumstances indicate that the items or services purchased will not be used in an exempt manner.